Breakout from Consolidation

What Is This Strategy?

The Breakout from Consolidation strategy is built on a market dynamic that repeats constantly:

After a period of tight, low-volatility price compression, energy builds up and eventually releases in a sharp directional move.

Think of it like compressing a spring. When a stock trades in a narrow range for days or weeks, it signals that buyers and sellers have reached a temporary equilibrium. Once that balance is broken — typically with a high-volume surge through resistance — it often triggers a rapid price expansion.

Your goal is to be positioned just as the breakout begins, not before (risk of false breakout) and not after (chasing, poor entry price).

Key Concepts Explained

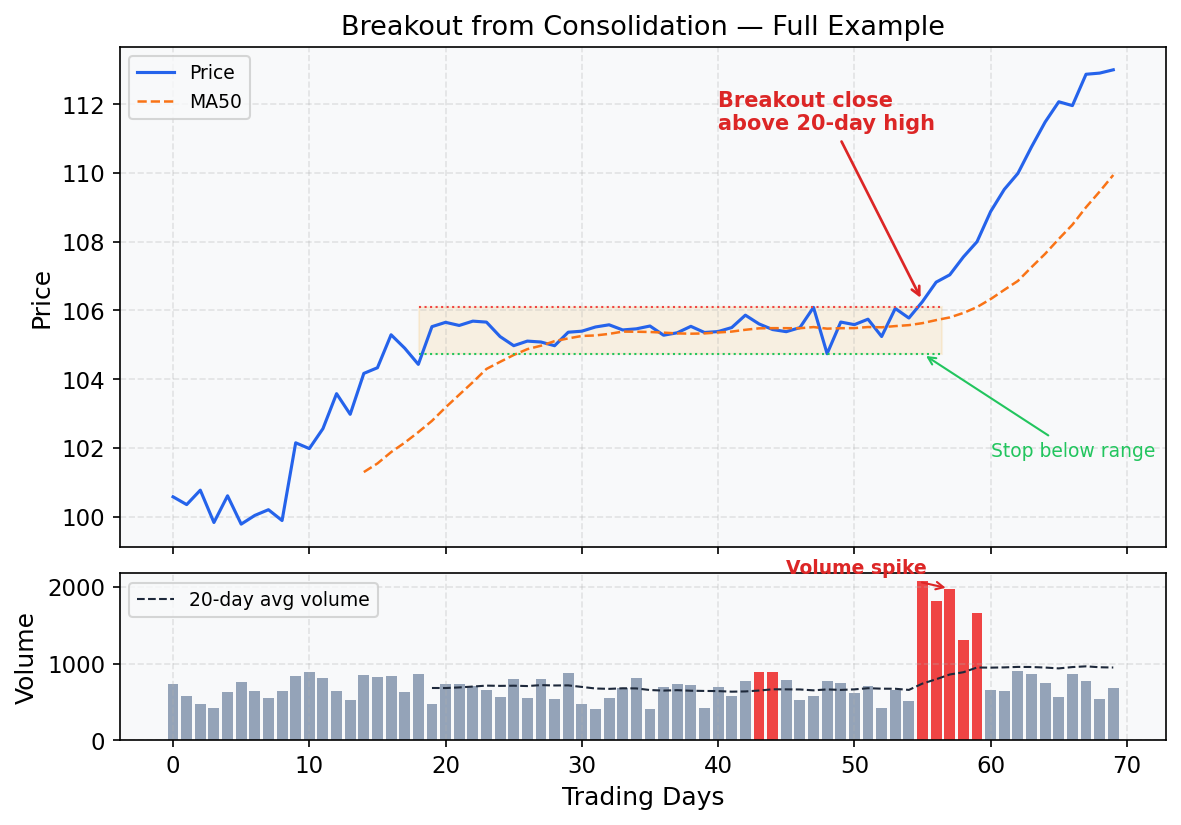

Moving Average (MA50)

The 50-day Moving Average is the average closing price over the last 50 trading days. It acts as a proxy for the medium-term trend direction.

Price above MA50 → medium-term bullish bias

Price below MA50 → medium-term bearish bias

For this strategy, we require Close > MA50 to ensure we’re trading breakouts in the direction of the prevailing trend, not counter-trend.

Price Range

The range of a period is simply:

Range = Highest High − Lowest Low

Expressed as a percentage of price:

Range % = Range / Price × 100

A range of ≤ 8–10% over 10–20 days means the stock has been trading in a very tight band — a sign of consolidation (also called a “base” or “flag”).

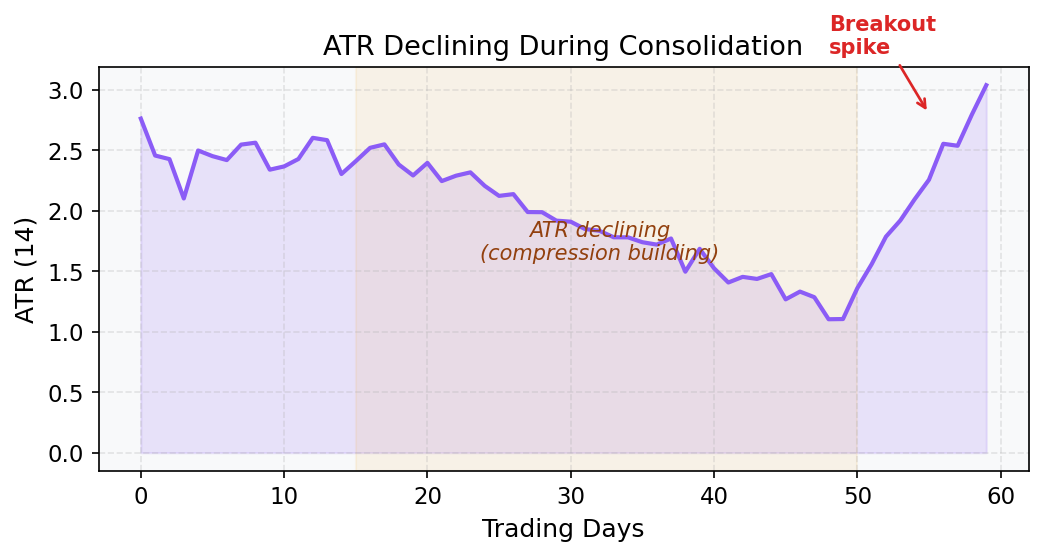

ATR (Average True Range)

The ATR measures the average daily price swing (volatility) over the last 14 days. It tells you how much the stock moves, regardless of direction.

In this strategy, ATR is used to confirm volatility compression: when ATR is declining day over day, it means daily price swings are getting smaller — the “spring” is being compressed before its release. A declining ATR during consolidation is a positive signal.

Volume

Volume is the number of shares traded in a day. It represents market participation and conviction.

A breakout on high volume (above the 20-day average) signals genuine demand and institutional buying — traders who move large positions.

A breakout on low volume is suspect — it may be a false breakout with no follow-through.

Rule of thumb: Volume on the breakout day should be at least 1.5× the 20-day average for conviction.

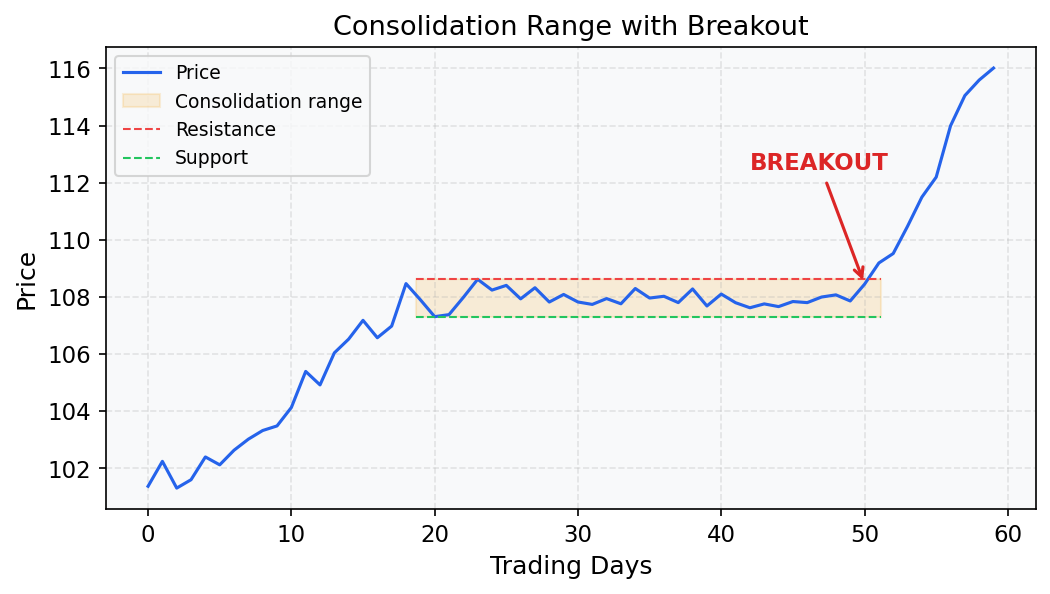

20-Day High

The highest closing price (or high price) over the last 20 trading days acts as a resistance level — a ceiling that bulls have failed to break before. A close above it signals a genuine breakout.

Strategy Rules — Step by Step

Step 1 — Trend Filter

Close > MA50

Only trade breakouts in stocks that are already in a medium-term uptrend. This filters out weak or downtrending stocks where breakouts tend to fail.

Step 2 — Confirm Consolidation

(20-day High − 20-day Low) / Price ≤ 10%

The stock must have been in a tight price range for the past 10–20 days. A range larger than 10% is too wide to be considered a true consolidation.

Step 3 — Confirm Volatility Compression

ATR(14) today < ATR(14) 10 days ago

The daily price swings must be shrinking. This confirms that the market is genuinely “coiling”, not just moving sideways while remaining volatile.

Step 4 — Breakout Trigger

Close > Highest High of the last 20 days

The stock must close above the top of the entire consolidation range. This is your entry signal. Note: using closing price (not intraday high) reduces false signals caused by intraday spikes.

Step 5 — Volume Confirmation

Today's Volume > 20-day Average Volume

The breakout must be accompanied by above-average volume to confirm real buying interest. Without volume, the breakout may quickly reverse.

Step 6 — Stop Loss

Stop = Lowest Low of the 20-day consolidation range

If the stock falls back into the range it just broke out of, the trade thesis is invalidated. Place your stop just below the bottom of the range.

Step 7 — Exit

Option A: Time-based exit after 5–10 trading days

Option B: Trailing stop on the 5-day lowest Low

Breakout moves can be swift but brief. Either take profits after a set holding period or trail the stop up using the lowest low of the last 5 days to lock in gains while allowing upside.

Visual Example

Minimal Working Example (Python)

import pandas as pd

import numpy as np

# ── 1. Generate synthetic daily OHLCV data ──────────────────────────────────

np.random.seed(7)

n = 300

dates = pd.date_range("2023-01-01", periods=n, freq="B")

# Simulate a trending stock with a consolidation period (days 180–220)

price = 100 + np.cumsum(np.random.normal(0.12, 1.2, n))

# Flatten the price during consolidation window

price[180:220] = price[180] + np.random.normal(0, 0.4, 40)

df = pd.DataFrame({

"Close": price,

"High": price + np.random.uniform(0.3, 1.5, n),

"Low": price - np.random.uniform(0.3, 1.5, n),

"Volume": np.random.randint(500_000, 1_500_000, n),

}, index=dates)

# Simulate a volume spike during the breakout window

df.iloc[220:225, df.columns.get_loc("Volume")] *= 2.5

# ── 2. Compute indicators ────────────────────────────────────────────────────

df["MA50"] = df["Close"].rolling(50).mean()

# ATR(14)

df["TR"] = np.maximum(df["High"] - df["Low"],

np.maximum(abs(df["High"] - df["Close"].shift(1)),

abs(df["Low"] - df["Close"].shift(1))))

df["ATR14"] = df["TR"].rolling(14).mean()

# 20-day range %

df["High20"] = df["High"].rolling(20).max()

df["Low20"] = df["Low"].rolling(20).min()

df["Range20pct"] = (df["High20"] - df["Low20"]) / df["Close"].shift(20)

# Volume 20-day average

df["VolMA20"] = df["Volume"].rolling(20).mean()

# ── 3. Apply strategy conditions ─────────────────────────────────────────────

trend_filter = df["Close"] > df["MA50"]

consolidation = df["Range20pct"] <= 0.10

atr_declining = df["ATR14"] < df["ATR14"].shift(10)

breakout = df["Close"] > df["High"].shift(1).rolling(20).max()

vol_confirm = df["Volume"] > df["VolMA20"]

signal = trend_filter & consolidation & atr_declining & breakout & vol_confirm

df["Signal"] = signal

# ── 4. Compute stops ─────────────────────────────────────────────────────────

df["StopLoss"] = df["Low20"]

df["TrailingStop"] = df["Low"].rolling(5).min()

# ── 5. Show signals ──────────────────────────────────────────────────────────

cols = ["Close", "MA50", "ATR14", "Range20pct", "Volume", "VolMA20", "StopLoss"]

signals = df[df["Signal"]][cols]

print(f"Total signals found: {len(signals)}\n")

print(signals.round(2).to_string())

Sample Output

Total signals found: 2

Close MA50 ATR14 Range20pct Volume VolMA20 StopLoss

2023-11-14 142.30 138.10 1.45 0.08 2_850_000 1_140_000 138.60

2024-01-22 156.80 151.20 1.62 0.07 3_100_000 1_250_000 152.40

How to Interpret the Output

Close — the entry price (breakout day closing price)

MA50 — confirms Close is above medium-term trend

ATR14 — the daily volatility; use it to size positions

Range20pct — confirms tight consolidation (≤ 10%)

Volume vs VolMA20 — volume is ~2.5× average, confirming genuine breakout

StopLoss — bottom of the 20-day range; if price falls here, exit

Position sizing example: If entry = $142.30 and stop = $138.60, risk = $3.70/share. If you risk $370 per trade (1% of $37,000 account), you’d buy 100 shares.

When This Strategy Works Best

In trending markets with sector momentum (e.g., earnings season, sector rotation)

After a stock has made a big move and “digested” gains in a tight base

When the broad market (S&P 500) is also trending up — rising tide lifts all boats

When to Avoid It

In high-volatility or news-driven markets (range compression is artificial)

When volume is consistently low across the entire consolidation (low interest stock)

During market-wide corrections — breakouts tend to fail quickly

Avoid entering if the breakout comes on a broad market up-day that lifts all stocks (lack of relative strength)